Co-signing on someone else’s private student loan isn’t a decision to make lightly.

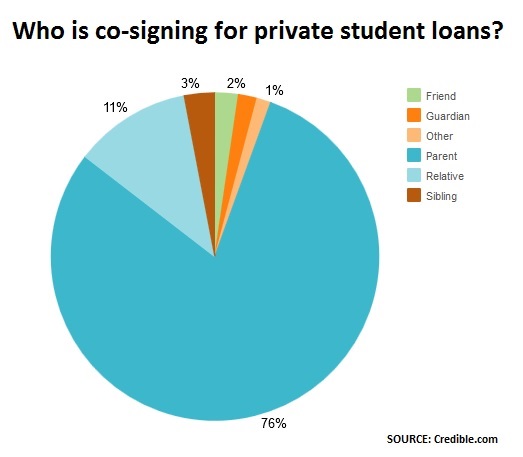

While parents represent three-quarters of co-signers, it’s not unusual to see others pitching in, according to a new report from private loan marketplace Credible.com, which assessed nearly 8,000 borrowers who requested a quote through the platform. Among loans with co-signers, 3 percent used a sibling, 11 percent another relative, and 2 percent a friend.

Having someone else lend their good credit can yield more affordable loans. Only 20 percent of undergrads applying on their own qualified for a personalized rate quote, Credible found, and they got an average loan rate of 7.46 percent. (Some offers were for fixed-rate loans, others, variable rates.) When undergrads applied with a co-signer, 51 percent qualified, and the average loan rate on offer was 5.37 percent.

But co-signing is risky. It ties you to that debt, meaning you could be responsible for the entire amount outstanding if the primary borrowercan’t — or won’t — pay up. Nearly 40 percent of co-signers found themselves on the hook for at least part of the bill, according to a June survey from CreditCards.com, and 28 percent saw a drop in their credit score from the primary borrower’s bad credit habits.

“A lot of people enter into these situations wearing rose-colored glasses,” Bruce McClary, a spokesman for the National Foundation for Credit Counseling, told CNBC.com earlier this year. “They’re not seeing reality where it is and the potential for things to go wrong.”

More reason to be cautious: Experts say a need for private student loans can mean that you’re overextended and the college selected isn’t a fit for your finances.

Leave a Reply